Do you want to use blockchain in your fintech app? In this article, we look at the key characteristics of this technology.

Cryptocurrencies took the world by storm: they’re among the defining technologies of the 2010s and, likely, the next several decades, along with smartphones. The key innovation behind cryptocurrencies is the so-called blockchain. In this article, we’ll look at blockchain in fintech and then transition towards analyzing the key ways to use this technology to boost the productivity of financial organizations.

What is the Place of Blockchain in Fintech?

Blockchain and fintech interact in at least two ways. Firstly, the blockchain is an essential part of all cryptocurrency operations. The blockchain is the key processing tool whenever you use Bitcoin or Ethereum to pay for something on the Internet. All fintech platforms integrating cryptocurrency inevitably have to interact with some form of blockchain. Secondly, blockchain technology is a potent upgrade path for future financial operations with traditional currencies. Blockchain technology has emerged as a transformative force in the field of fintech. Its decentralized and transparent nature provides enhanced security, efficiency, and trust in financial transactions. Blockchain has the potential to revolutionize various aspects of fintech, including payments, remittances, smart contracts, and identity verification, making it a crucial part of the industry’s future.

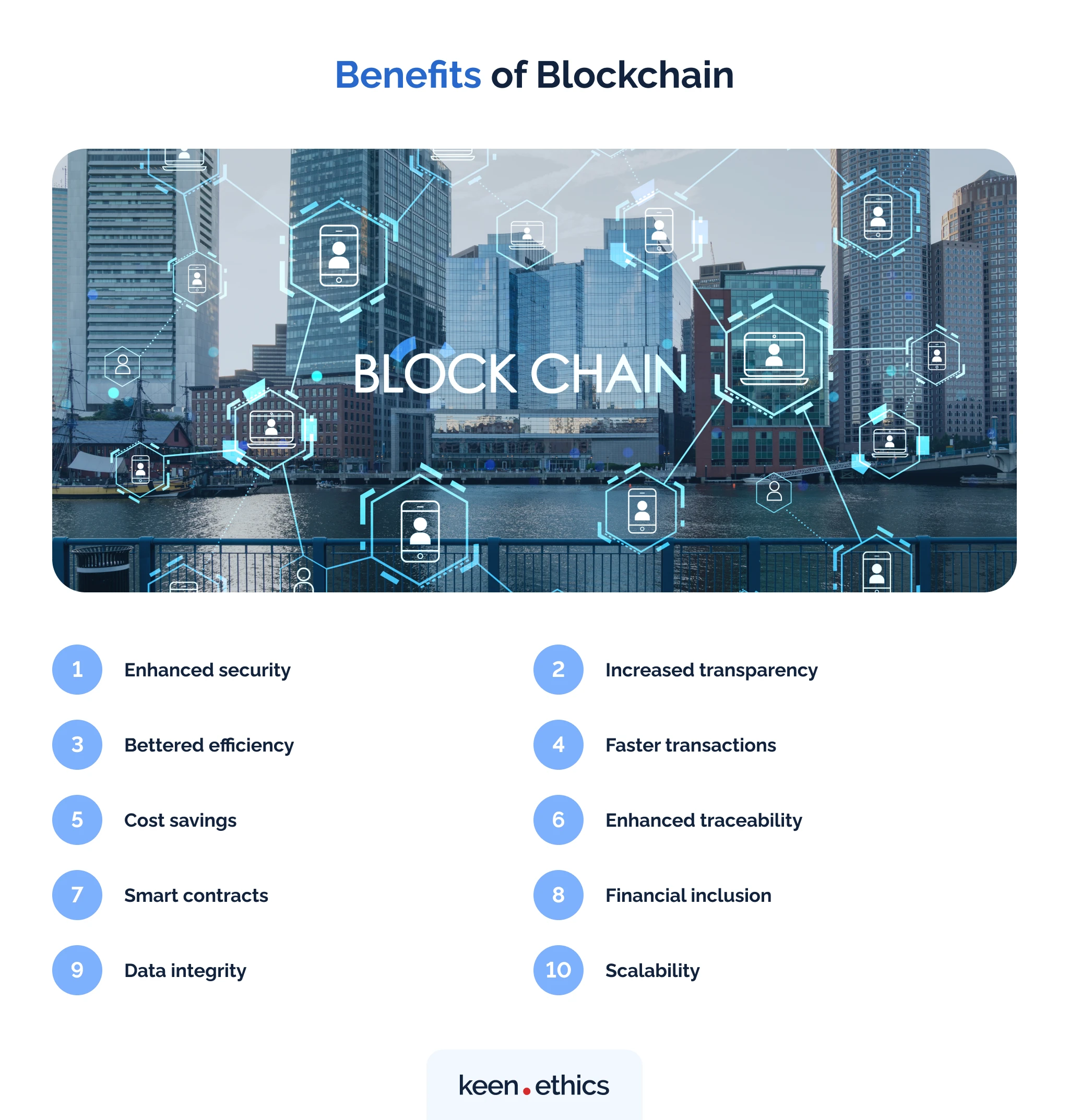

Benefits of Blockchain

Blockchain and fintech will likely produce promising innovations in the banking sector. Why is that so? In our opinion, the key reason stems from the unique characteristics of blockchain, which offers major advantages to financial institutions and the average users. Here are some of the key positives the blockchain technology provides:

- Enhanced security: blockchain’s decentralized and cryptographic nature ensures secure and tamper-proof financial transactions. This aspect of the technology reduces the risk of fraud and unauthorized access.

- Increased transparency: the transparent and immutable nature of blockchain enables real-time visibility of transactions. In this light, it’s possible to trace any activity: such an approach is crucial for enhancing trust among participants and reducing the need for intermediaries.

- Bettered efficiency: blockchain eliminates the need for manual reconciliation and paperwork, streamlining processes and reducing costs associated with traditional financial systems. Everything that has to do with blockchain is, more or less, automated.

- Faster transactions: blockchain makes transactions extremely fast. After all, there’s no need for human input during the transaction processing stage.

- Cost savings: By eliminating intermediaries, minimizing paperwork, and streamlining processes, blockchain can reduce transaction costs in fintech. Blockchain in fintech is a perfect opportunity to automate many routine tasks and direct the workforce towards more complex processes, such as fraud detection.

- Enhanced traceability: blockchain is an example of a so-called distributed ledger. It uses independent computers to record, share and synchronize transactions in their respective electronic ledgers (instead of keeping data centralized as in a traditional ledger). Why is this important? Financial organizations are often used for money laundering. Indeed, cryptocurrencies became a major payment method for criminals in the 2010s due to their novelty. Nonetheless, blockchain ensures easier tracking of financial transactions than traditional payment methods. With proper institutional oversight, it can ensure the strongest compliance with the regulations.

- Smart contracts: blockchain encourages self-executing smart contracts, automating contract enforcement and reducing the need for intermediaries. Theoretically, blockchain in fintech can help create a world with minimal fees for banking services.

- Financial inclusion: blockchain technology enables access to financial services for the unbanked and underbanked populations. Why is this significant? This technology can promote financial inclusion and economic empowerment in developing countries. The use of custom cryptocurrencies proved to be a major success in African countries, facilitating the development of local economies, as data from the IMF implies.

- Data integrity: blockchain ensures data integrity and prevents unauthorized modifications, making it reliable for storing and transferring sensitive financial information. Changing the data in the blockchain is virtually impossible, making transaction information easily traceable for both the users and the relevant control-centric institutions decades after certain actions.

- Scalability: with advancements in blockchain technology, solutions are being developed to address scalability concerns, allowing for increased transaction throughput in fintech apps.

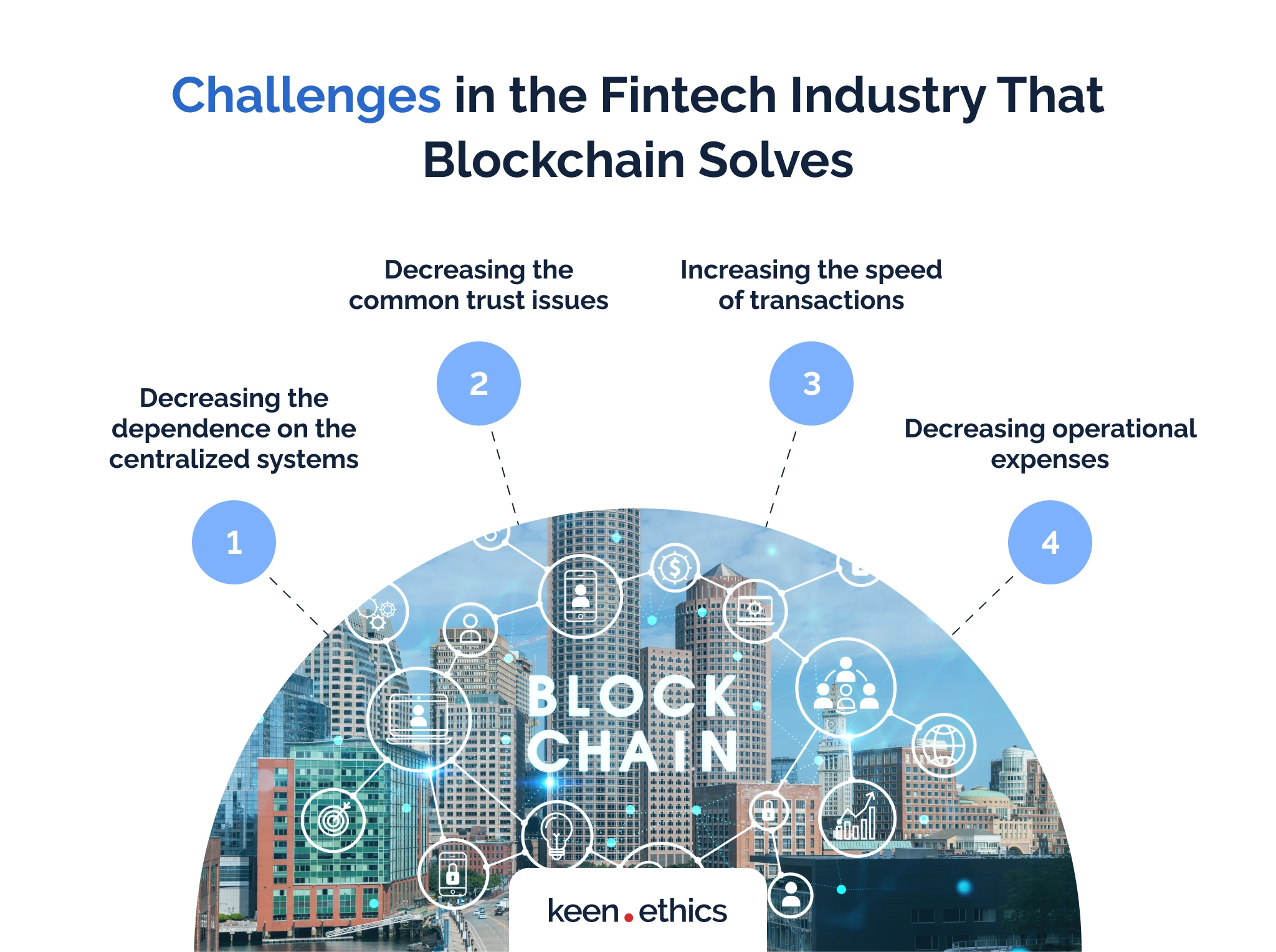

Challenges in the Fintech Industry That Blockchain Solves

Blockchain & fintech integration offers many benefits for the long-term stability of the fintech sector. What are those? Let’s look at the challenges blockchain can solve regarding the modern fintech sector. As you’ll see, the long-term benefits of this revolutionary technology are tremendous:

Decreasing the dependence on the centralized systems

A key problem for many financial organizations is having some form of headquarters. Most financial calculations occur in one place (for instance, a cluster of servers). This model has major downsides: servers are expensive to host, and, more importantly, there’s always the risk of some disasters disrupting the long-term stability of the financial sectors. For instance, we know large-scale hacker attacks previously led to long-term disruptions in the functioning of financial services. The blockchain solves this problem once and for all. The majority of the activities within it are decentralized. One can distribute calculations among multiple users, preventing situations in which the disruption of one server renders a service unusable. With blockchain, clients can use reliable fintech services from any location. IBM sees this technology as a strong solution for disaster management.

Decreasing the common trust issues

The blockchain solves the issue of trust via its decentralized and transparent nature. In a blockchain network, multiple participants verify and record transactions through a consensus mechanism. Once a transaction is validated and added to the blockchain, it becomes immutable. No person (even the creator of the blockchain network) can alter the relevant records. This creates high trust in the system, as all participants have access to the same verified information. The transparent nature of blockchain allows participants to independently verify the authenticity and integrity of transactions. This approach is crucial for eliminating the need to rely solely on trust in intermediaries or centralized entities.

Increasing the speed of transactions

One of the key blockchain fintech use cases is the improvement of banking system efficiency. What’s the problem with the traditional systems? Despite a significant degree of automation, they still demand a major emphasis on human labor. Many transactions require manual analysis to ensure the absence of large-scale issues. In this regard, blockchain in fintech is a promising technology because it solves this common problem. Modern blockchain frameworks leverage key innovations to ensure the highest degree of progress for the users. In many situations, the speed of transactions based on a blockchain depends solely on the speed of the existing devices. This means the usage of innovation in the fintech sector can improve financial service speed. Many operations will become instantaneous, even if one has to send funds to distant foreign countries.

Decreasing operational expenses

The problem with the current financial system is that it relies on people to do work, which costs a lot of money. Training a high-quality specialist for the banking sector isn’t easy. The relevant individuals must have higher education and know how to work with the specific hardware and software of the involved financial organization. In this light, the payment for the banking labor force has to be high to decrease the probability of turnover. The problem with such an arrangement isn’t only about payment. Many talented people have to work on tedious and monotonous tasks in traditional systems. Blockchain resolves this problem once and for all: it automates most transaction-oriented tasks. Moreover, it frees the workforce, allowing managers to offer talented individuals jobs with greater creativity. This approach is crucial for decreasing the operational expenses. With blockchain technology in fintech, one can lower expenditures on various operators and invest more in analytics and customer experience improvements. Chris Trew writing for AIThority notes that blockchain will be the basis of automation in the future.

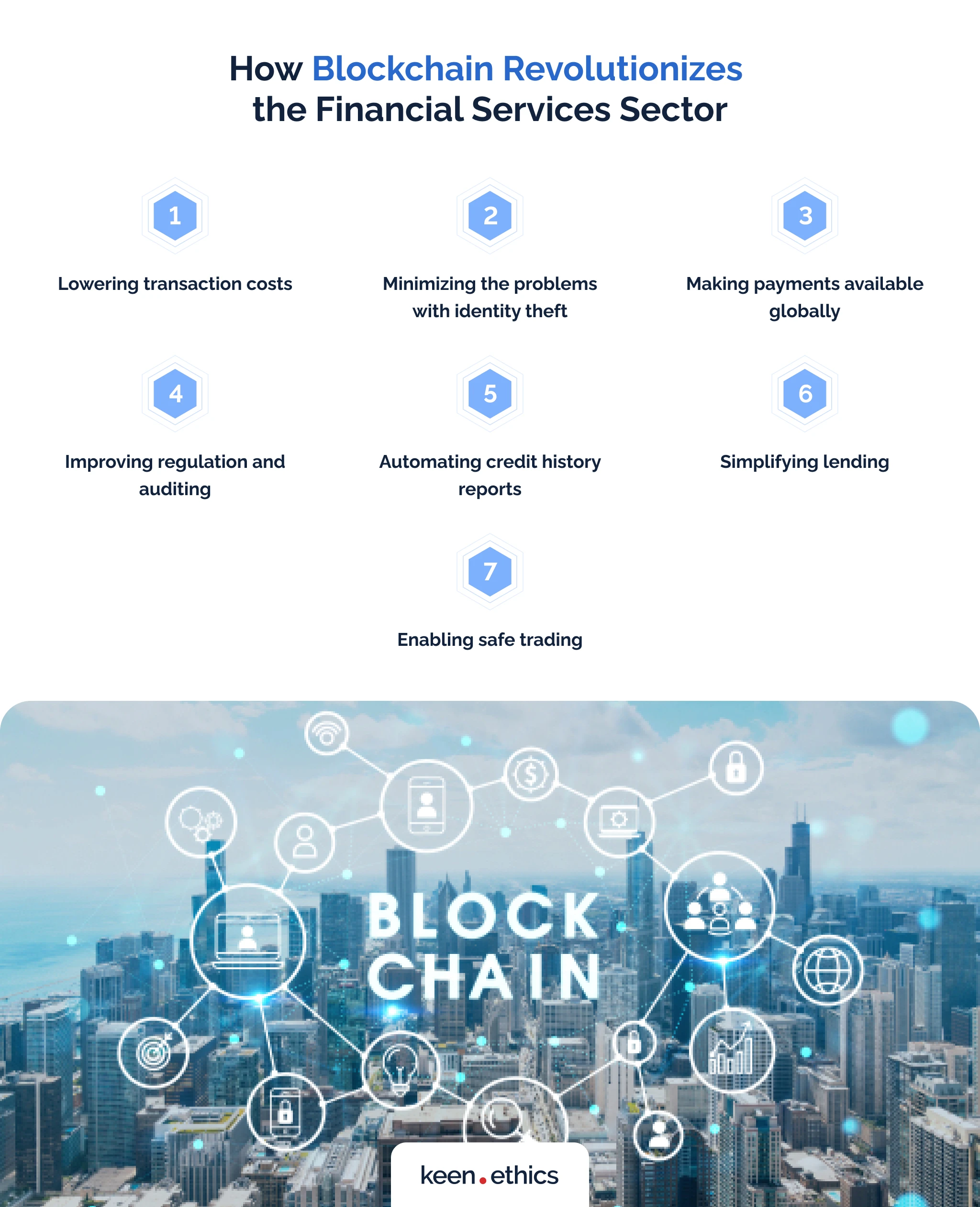

How Blockchain Revolutionizes the Financial Services Sector

Blockchain in the fintech industry will likely become essential for most companies. How exactly does blockchain revolutionize financial services? Let’s review the key positives that the technology can bring about in long-term scenarios:

Lowering transaction costs

A major problem for traditional financial services is the reliance on human operators. While modern tools automate many tasks, some human input is necessary to ensure the proper functioning of financial services. Blockchain reduces the need for worker input to a minimum. We know many cryptocurrency platforms that automate the majority of transaction-related tasks. In this context, the only service necessary is support for potential bugs and some user questions. This approach is crucial for lowering expenditures on transactions. If there are fewer workers involved in each transaction, it’s possible to reduce their financial impact.

Minimizing the problems with identity theft

Blockchain minimizes difficulties with identity theft by delivering a secure and tamper-proof system for identity verification. Instead of relying on traditional centralized databases vulnerable to breaches, the blockchain utilizes cryptographic techniques to store and validate identity information. Each user has a unique digital identity stored on the blockchain. The specialists can verify it through cryptographic proof. This decentralized approach eliminates the need for users to share their data with multiple parties, reducing the risk of breaches. Ideally, only the users involved in a transaction would know details about each other. Besides, blockchain’s transparent nature allows individuals to have reinforced control over their identity. What does this entail? Such technology allows them to selectively share information while maintaining their privacy and minimizing the chances of identity theft.

Making payments available globally

Have you ever tried sending funds between different countries? Even if they have major cooperation agreements, such a process is expensive and takes a long time. One of the key blockchain use cases in finance is making payments global. Blockchain doesn’t need any banking institutions to ensure the transition of funds. This means one can send money from any location. We know cryptocurrencies allow people in Africa, for example, to send funds to the United States without major barriers. This is why blockchain is such an important milestone for the financial sector. It offers a pathway for the first borderless system of transactions. With blockchain, financial borders will finally be destroyed.

Improving regulation and auditing

Blockchain improves regulation and auditing by providing a transparent and immutable ledger of transactions. Regulators and auditors can access the blockchain to verify and audit financial activities in real time. The distributed nature of blockchain ensures all participants have access to the same verified data. This factor is crucial for reducing the risk of fraudulent reporting or manipulation. Moreover, smart contracts on the blockchain enforce regulatory compliance automatically. In this way, one can ensure that transactions adhere to predefined rules and regulations. Why is blockchain such a significant technology for the financial sector? It not only automates many tedious tasks, but also enables an easier pathway for preventing the breach of regulations.

Automating credit history reports

Among the big blockchain fintech use cases is the usage of the technology for automating credit reports. In the modern world, many banks already have automatic frameworks for this goal. The key problem with them is the accuracy of information. Traditional banking models have a negative tendency: it’s easy to push fake information about the users into them. In this respect, blockchain boosts the ability to automate credit reports. How exactly? This framework decreases the amount of fake information about user transactions. Moreover, it boosts their visibility, making it impossible to hide their credit history by, for instance, using illegal microfinance organizations. Such an approach enables one to create credit reports of the highest quality for the clients.

Simplifying lending

Blockchain simplifies lending by removing the need for intermediaries and streamlining the loan process. Using blockchain technology to lend money, people can interact with each other without banks or other financial institutions. Smart contracts on the blockchain automatically enforce loan agreements, eliminating the need for extensive paperwork and manual verification processes. The transparent and immutable nature of blockchain also helps establish trust between parties, reducing the risk of fraud. Now, it’s possible to lend outside the traditional financial organizations and, moreover, properly enforce the relevant contracts. Blockchain increases freedom for the users and decreases the risks for all parties.

Enabling safe trading

The aforementioned advantages, such as smart contracts and transparency, enable another benefit for the use of blockchain in fintech. What is it? Blockchain is perfect for trading. With this technology, it’s safe to make small transactions regarding things we use daily and even some serious investments, such as real estate or company shares. The innovation makes trading fast and decreases the risks for all involved parties.

Best Blockchain Use Cases in Fintech

We know of multiple notable blockchain use cases in finance. Here’s the description of the key cases that are of interest:

Ripple

Ripple utilizes blockchain technology to enable fast and low-cost cross-border payments. Its payment protocol, XRP Ledger, allows financial institutions to finalize transactions instantly. This approach reduces the reliance on traditional correspondent banking networks and minimizes liquidity requirements.

Circle

Circle uses blockchain technology to power its stablecoin, USDC (USD Coin). USDC is a digital currency pegged to the US dollar, enabling fast and borderless money transfers with transparency and audibility. It provides a stable and reliable medium of exchange for individuals and businesses in the digital economy. Using this stablecoin, one can send dollars to any part of the world without barriers.

Chainlink

Chainlink leverages blockchain to enhance the reliability of data used in smart contracts. By connecting blockchain networks with real-world data sources, Chainlink ensures smart contracts can access accurate and trustworthy information. This approach enables the execution of complex financial agreements such as insurance claims, loan agreements, and derivatives contracts.

Veem

Veem utilizes blockchain to streamline global payments for businesses. By integrating blockchain technology into its platform, Veem offers secure and cost-efficient cross-border transactions with real-time tracking, transparent fee structures, and simplified reconciliation processes. Ultimately, it eliminates the need for intermediary banks. Using these tools, the company finds a way to reduce costs and improve the speed of international payments.

Celsius Network

Celsius Network was a cryptocurrency-based business that used blockchain to provide decentralized lending and borrowing services. Through its platform, individuals could lend their cryptocurrencies and earn interest or borrow assets using their digital holdings as collateral. Regrettably, Celsius Network became bankrupt in 2022 due to mismanaging its investments during the cryptocurrency boom of 2020-2021, according to CoinDesk. The company got too optimistic regarding its prospects, failing to consider the stabilization of the Bitcoin price to around 20000 dollars per unit. Nonetheless, the company proves blockchain is feasible for various financial sectors. With better regulatory oversight and a stricter approach to fund management, one can expect that blockchain in the fintech industry will overtake the lending market. Celsius Network involved a strategy-related failure instead of a concept-related one.

Conclusion

All in all, blockchain is likely the future of the fintech market. This technology offers a perfect pathway for improving the existing practices in the banking sector. It can speed up transactions and boost their security level. Do you want to invest in this technology? Addressing our company makes sense in such a case: we have experience developing high-quality financial solutions.

FAQ

What types of blockchains exist?

Public, private, and consortium blockchains are the three main types of blockchains that exist.

What blockchain technology do you recommend for fintech?

Public blockchains, such as Ethereum or Stellar, are recommended for fintech due to their established infrastructure and wide range of smart contract capabilities.

How to install blockchain within a fintech app?

To install blockchain within a fintech app, developers must integrate blockchain libraries or APIs and configure the app to interact with the desired blockchain network.

What categories of fintech exist?

Categories of fintech include payment and remittances, lending and borrowing, personal finance management, insurance technology (insurtech), and wealth management.

How do blockchain and fintech differ?

Blockchain is a technology providing a decentralized and transparent ledger, while fintech refers to the use of technology in financial services to enhance efficiency, accessibility, and innovation.

In that case, don’t hesitate to contact us for a free estimate of your project.