Embedded finance is among the strongest trends in the modern app development market. This article reviews the trend and some key success cases.

Before we define embedded finance, let’s first look at the importance of financial services for modern civilization. Financial services are an essential part of everyday life for the majority of us. If you don’t participate in the monetary economy, your life is likely to be difficult and poverty-stricken. The only people living outside of it are isolated subsistence farmers in developing countries and various hermits. Everyone else engages in trade in one way or another. This trade is impossible without the presence of banks, which produce (in case of state-oriented organizations) and manage funds. Considering that finance is already a central component of our lives, it’s reasonable to make it as comfortable for the users as possible. Embedded finance is among the technologies enhancing comfort for the relevant users. It allows streamlining many purchases and makes them seamless. In this article, we’ll review the embedded finance definition, look at the examples of embedded finance usage, and outline the key advantages and disadvantages of the concept.

What Is Embedded Finance?

Embedded finance is a term used to describe the integration of financial services and products into non-financial platforms or businesses. It represents a growing trend in the financial technology (FinTech) industry, where financial services are offered seamlessly within the context of other industries or apps. What do we mean by the “integration of finance services and products into non-financial platforms or businesses”? Let’s imagine you want to purchase a MacBook online from a web shop, but you don’t have enough money at hand to do this. Many webshops solve this problem by embedding money-lending services into their sites. What can you do in this situation? You can take out a loan from a partnering banking organization and repay your laptop in 12 or 24 months, for instance. This situation is a perfect outline of the so-called embedded finance. The key goal of embedded finance is the maximum convenience for the client.

How Does Embedded Finance Work?

Embedded finance doesn’t have any complex models behind it. A typical framework is that a banking/finance organization contacts a company (store or booking site) or vice versa to offer an embedding contract. Usually, it doesn’t imply any major payment for the integration due to the additional benefits. Both parties have significant reasons to enter these contracts. On the one hand, shops and other merchants get an additional framework for attracting new clients. If they get insurance without barriers or pay for some devices in parts, the likelihood of a successful purchase rises. On the other hand, banks and other financial organizations get to attract users to their unique services through the products of a partner shop or service. Upon “subscription,” an organization selling a product or service can offer banking or insurance as an additional option for the clients. In short, embedded finance should be easy to set up for the majority of organizations. In fact, many banks and insurance organizations even go as far as to include simple integration APIs, which make cooperation especially easy. The approach is a viable business model: we know some banks, such as the German Solaris, have major contracts with Samsung, Coinbase, and American Express services.

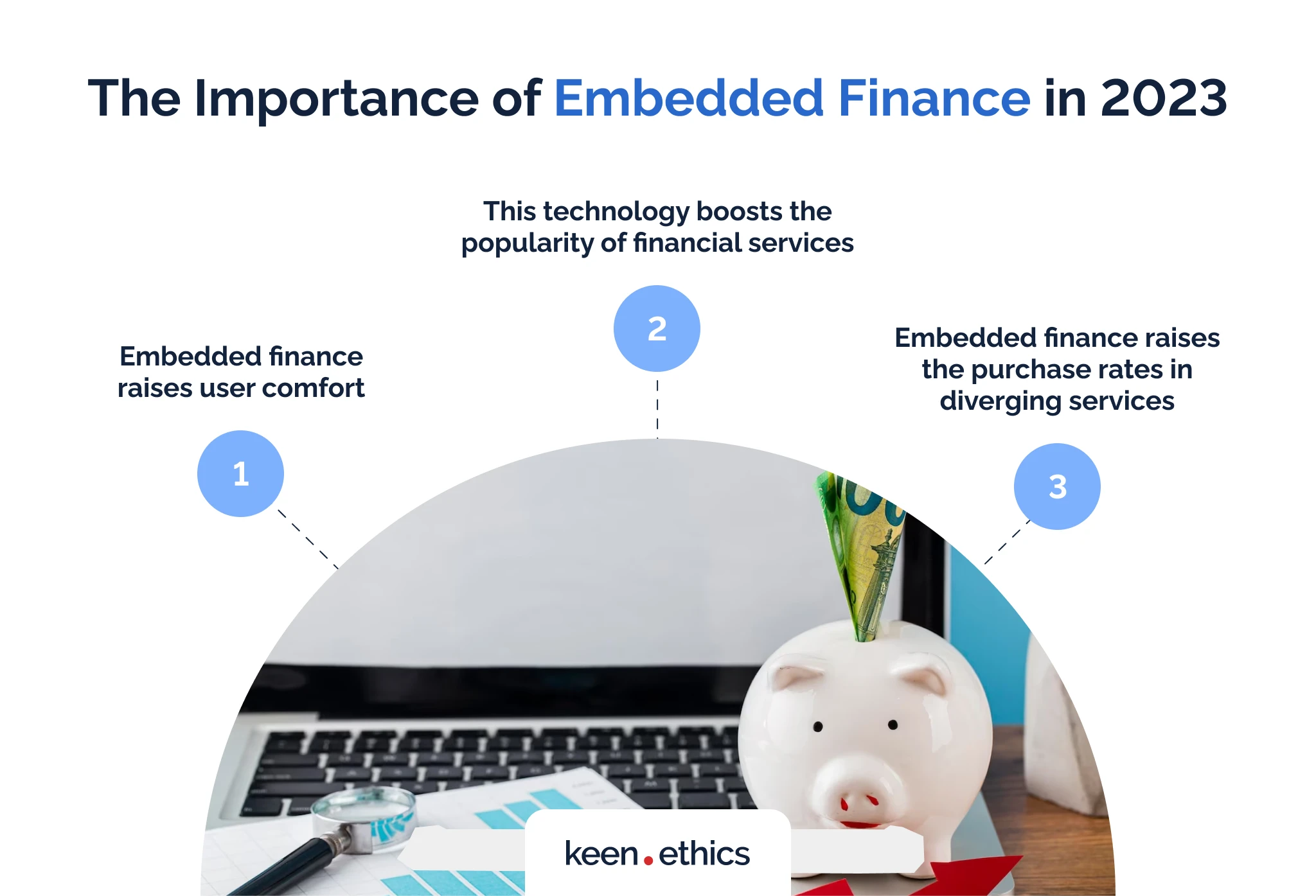

The Importance of Embedded Finance in 2023

In our opinion, embedded finance is vital in 2023 for multiple reasons. Here are some of them (some are relevant for the clients, others for banks):

- Embedded finance raises user comfort. Using embedded finance, an average client of a tourist site or device shop gets an opportunity to lessen the amount of time they spend on additional financial services. For example, a tourist wouldn’t have to search for an insurance company if its services are already a part of a tourist site. In turn, a person who wants to purchase a professional course wouldn’t have to search for financing from outside sources. Instead, one can get it from an organization approved by the course creators. We know the rising cost of living in the preceding several years is driving more and more people towards embedded finance, according to Fintech Nexus experts;

- This technology boosts the popularity of financial services. Many people don’t know about the full spectrum of opportunities in the finance market. For instance, individuals in countries with universal health coverage rarely consider health insurance, even though it can make their healthcare experience more comfortable. Embedded finance solves this coverage problem once and for all. How exactly? It informs the users of diverging services (for instance, course-centric education websites) that they have unique opportunities. Individuals who want to buy expensive smartphones are likely to reconsider their decision to wait and save funds when they see lucrative loan opportunities;

- Embedded finance raises the purchase rates in diverging services. The final positive of this innovation is the ability to offer major benefits for non-financial services. Many people avoid tourism or don’t buy expensive items because finding funds or getting insurance is difficult. Embedded finance allows integrating those services in several clicks. Considering how easy such decisions are, more people are likely to use diverging non-financial services with the rise of relevant innovation. For example, shops that sell expensive clocks can expect a higher rate of purchases when more potential customers are able to take out loans for their products. If you want to increase the coverage of the market, embedded financial technologies are a perfect choice.

How Embedded Finance Is Shaping the Financial Sector

Embedded finance is revolutionizing the financial sector by integrating financial services directly into non-financial platforms. This factor is important for two reasons. Firstly, this seamless integration allows users to access banking, payment, and insurance services without leaving their favorite apps or websites. Such an approach maximizes the engagement of potential customers and promotes a comfortable user experience. With the advent of embedded finance, more people are likely to have a positive attitude toward financial services. Embedded finance also extends financial services to a wider audience, including those previously underserved, promoting financial inclusion. As we’ve mentioned before, innovation offers benefits for clients, shops, and banks. Secondly, embedded finance improves our understanding of customer behavior. It offers tremendous volumes of information that helps us understand the everyday needs of the clients and predict their purchasing behaviors. By leveraging the data from the embedded finance integration, financial institutions offer personalized solutions, enhancing customer satisfaction.

Still, there’s also a major downside stemming from the implementation of the embedded financial services. What is it? In our opinion, the key problem is the expansion of directions for cyberattacks. Instead of caring about internal banking or insurance websites, modern businesses now need to pay attention to multiple frontends. This situation demands careful attention to data security and privacy concerns to ensure the continued trust and success of this transformative trend in the financial industry. To embed the banking or insurance services into other sites, one needs to write new code, which creates major concerns for long-term security. Embedded finance is lucrative, but it also requires new expenses to ensure long-term security.

Various Types of Embedded Finance

What is embedded finance? It’s a field with massive opportunities. Many types of apps are possible on the market. Here are high-quality ideas for creating an embedded financial app:

Payment Integration

What’s the key issue of selling something on the Internet? You have to ensure a comfortable framework for payment: cash can’t work in this case. In this light, one of the most common embedded banking approaches arises. What does it involve? Integrated payment for diverging services. If you’ve ever paid for any product with a credit card or PayPal on the Internet, you’re likely to be familiar with this usage of technology. How does it work? You choose checkout, and then an integrated payment service allows you to enter credentials and send the funds to the vendor. Many banks offer their frontends for such a service. In this regard, you have multiple options, which we recommend ranking according to the relevant fees and security they offer.

Banking as a Service (BaaS)

Another way to embed the services for the clients is to offer advanced banking functions within a non-financial app. This approach is common for real estate or time management apps cooperating with other banks to deliver high-quality service to their customers. The idea is simple: non-financial businesses partner with banks to give banking services, like savings accounts and loans, to their clientele. Why does this work so well? Many non-financial apps are discipline-oriented. Their whole idea is to help certain people become better. For instance, an organizer app benefits from the integration of savings services because it already seeks to bring order into the life of a person. Rationality doesn’t equal intelligence: this means the integration of banking services into a time-tracking app can push many individuals to revise their money habits. An efficient worker may be bad with money. Many people work 12 hours a day to then spend all the funds on entertainment. If you offer people to save funds via embedded services, you can transform their lives and make the outcomes of the long-term work more meaningful.

Buy Now, Pay Later (BNPL)

A common problem for many people is that they don’t have enough money at hand to purchase certain things. Some people put all their funds into saving and can’t buy something immediately due to the account rules. Others have large expenditures and, as a result, can’t make any significant savings to purchase something in one installment. In this regard, the Buy Now, Pay Later model is a great solution for many platforms selling certain products and services. How does this approach work? The BNPL framework permits the customers to purchase items and pay for them in installments, making it easier to afford products and boosting sales. For example, if you need a MacBook for work but don’t have funds for it, the presented model is a great solution. Instead of paying 999 dollars in one installment, you can split the payment between 12 months. Many BNPL frameworks are notable for their low-interest fees. In this light, the customer won’t overpay as much as many people may think with these frameworks.

Insurance within Reach

Embedded financial services aren’t only about finances. They also allow one to try out high-quality insurance. Many people who buy tourist services online or want to purchase a car need insurance opportunities. In the past, buying on the Internet was more difficult because you had to find the services personally. With modern approaches, this changes once and for all. Many insurance services have great sites that even calculate risks based on user data. This means integrating the capabilities in the key websites isn’t a problem for many developers. All you have to do is create a separate module for the non-financial websites to use. Why is this technology so important? In our opinion, it’s relevant because it empowers businesses to provide insurance coverage directly through their platforms, simplifying the process for customers and safeguarding their interests. The ability to purchase insurance immediately is liberating regarding time and better for safety due to pushing the clients into considering insurance in the first place.

Practical Embedded Finance Examples

What are some examples of embedded financing in real-life scenarios? Here are the key firms you need to consider:

Shopify

Shopify is one of the largest platforms for creating and managing web-based stores. Apart from focusing on the main function: providing high-quality web platforms, Shopify also offers a strong embedded web service. This company is notable for delivering Shopify Capital, a platform that gives financing to small business owners who use their ecommerce platform. This embedded finance solution allows business owners to receive funding for their business without having to leave the Shopify platform. Why is this important? While the conditions in Shopify Capital may not be the best on the market, it offers great comfort for the users. Many business decisions have to be fast and close to spontaneous. Shopify Capital enables people to make such decisions by allowing business specialists to get money for their business ideas in several clicks.

Square

Square is a large payment solutions system for small businesses. The company also has some embedded finance tools to assist clients with managing their everyday finances. What exactly does this company do? They have a suite of financial tools that integrate with their point-of-sale system. Using it, the relevant business experts can manage and get funds necessary for their day-to-day operations. So, what does Square embed for its customers? The key services include things like payroll management, invoicing, and lending. Why is this all so important, in our opinion? What’s the reason to use Square’s embedded services? They’re vital due to allowing small business owners to manage their finances all in one place. Such an approach helps with maximizing the efficiency of the relevant business. Many opportunities require fast funding. By having a unified platform, you can make almost real-time choices to purchase certain goods.

Stripe

Stripe is another large-scale payment processing business on the global market. It helps with a tremendous number of transactions. This isn’t the only embedded finance service provided by Stripe. The company is also notable for Stripe Capital, a lending service that gives loans to businesses using its payment processing platform. This allows businesses to access funding quickly and easily. More importantly, they can offer the presented lending services to their customers together with payment processing. In this way, Stripe allows maximizing income on high-priced products by enabling the clients to buy in installments, for example.

Intuit

Intuit is one of the largest platforms for financial management. It allows reviewing tax information and credit histories, for instance. Ultimately, the service is also perfect for processing aspects such as payrolls. Still, this element of the business isn’t about embedded finance. What is meaningful here is that Intuit provides QuickBooks Capital, a lending service offering loans to small businesses based on their QuickBooks data. This allows business owners to easily access funding without having to spend time filling out lengthy loan apps. Obviously, the service is perfect for integrating Buy Now, Pay Later frameworks.

PayPal

PayPal is among the largest services for integrating multiple credit cards. It’s the best framework for payment on the Internet, along with Google Pay and Apple Pay. So, what can PayPal offer to its business partners? They have a range of financial tools that integrate with their payment processing platform, including invoicing, business loans, and debit cards. This allows small business owners to manage their finances easily and securely.

Overall, embedded finance is becoming more common as companies investigate how to provide financial services to their customers without having to leave their platforms. These examples involve just a few of the many companies that are offering such solutions. As you may see, a clear trend is present here: lending is among the most common use cases for embedded finance. Many people like such services because they’re perfect for enhancing one’s lack of income in the current fund-starved economy.

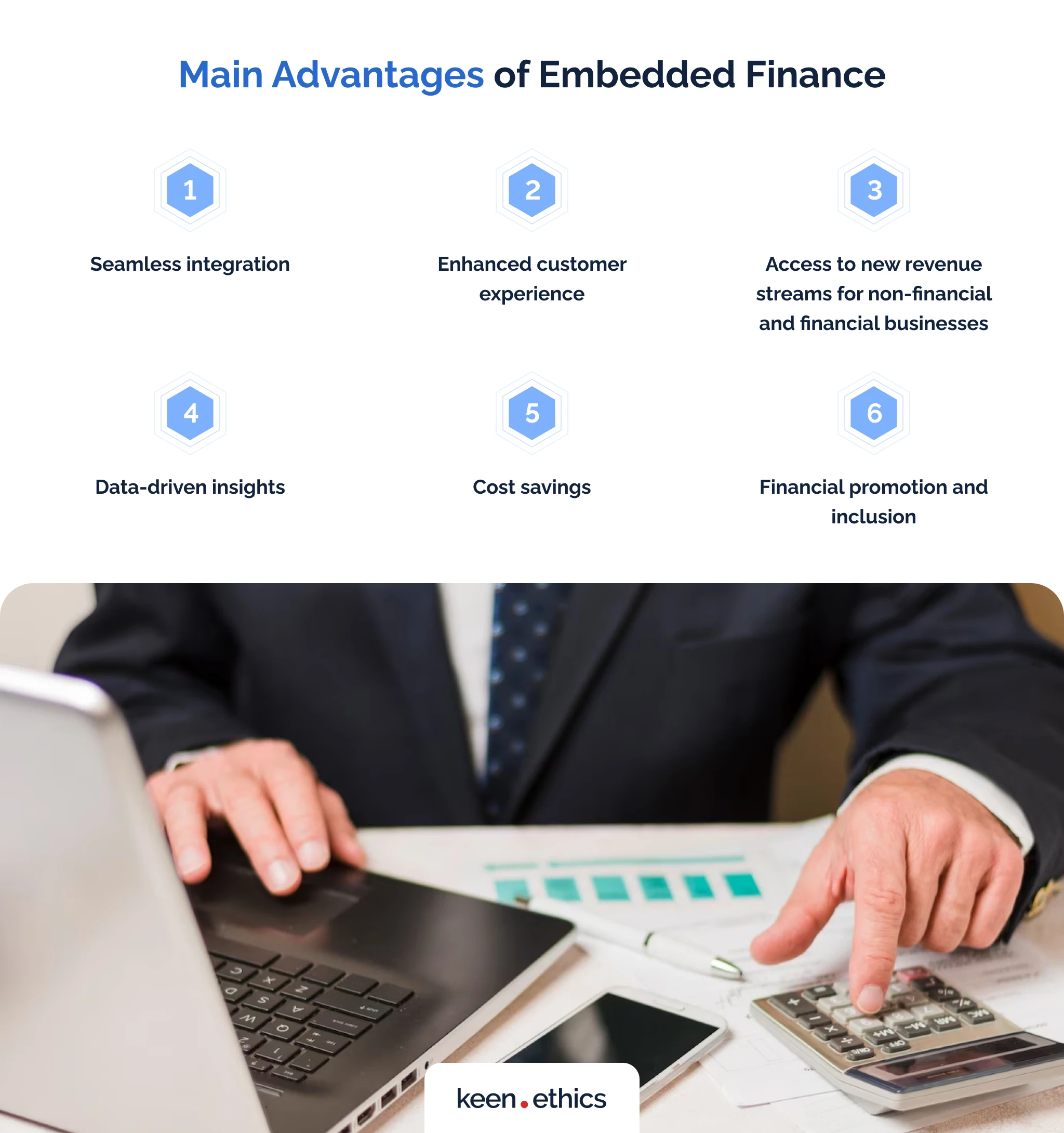

Main Advantages of Embedded Finance

Now that we know the key types of embedded finance, it’s time to look at the benefits of the presented technology.

Seamless Integration

The key advantage of using embedded finance is the seamless integration with diverging websites. A major problem for many financial services is that they’re separate from different trading platforms. Banks used to provide services for organizations selling some goods, but they had to isolate all the paperwork from the customers. Embedded finance solves this problem once and for all. When a person decides to buy something or take out a loan, they get an opportunity to do these actions directly within the interface of a bank. What is embedded finance about? It’s about the integration of banking services and their frontends directly into other sites. The integration is indeed seamless: there’s no need to visit any websites of banking organizations. Why is this so important? This step is about respect for the user. If you help save time, the users will respect both the banking website and the non-financial organization more.

Enhanced Customer Experience

Embedded finance isn’t about comfort and being seamless alone. It can also enhance the long-term experience of the user. How exactly? For instance, ecommerce platforms offer instant loans for purchases, making it convenient for customers to make bigger transactions. Many people who have their businesses invest the majority of their funds. They don’t have large reserves to maximize the long-term influence of their resources. In this light, the embedded finance growth is the new normal on the market. Businesses get an opportunity to purchase certain products by immediately taking out loans for them. This customer experience is superior for non-business clients too. How exactly? Having an opportunity to buy the things people want without waiting for a salary is liberating in a financial sense. More mundane approaches such as integrated payment also are rational from the standpoint of user comfort. The ability to pay with a credit card or services such as Google Pay makes the user experience comfortable through the aforementioned seamless approach.

Access to New Revenue Streams for Non-Financial and Financial Businesses

As we’ve mentioned before, embedded finance is beneficial to all parties enabling this technology in their core services. On the one hand, embedded finance integration enables non-financial businesses to create new revenue streams beyond their core offerings. A store selling Apple products can, for example, start getting revenue from low-income individuals as they would be able to take out loans for the new devices. This means they get a chance to boost their audience. On the other hand, banks and other financial organizations also receive a major set of benefits. They get to earn more commissions, fees, or interest from the financial products and services they promote by targeting a larger audience. In short, both the banks and the non-financial organizations they work with can expand their audience via embedded finance.

Data-Driven Insights

The income-centric benefits of embedded finance are obvious: better user experience leads to better market coverage and higher incomes. Still, there’s a major benefit that experts don’t mention as commonly. Embedded finance generates valuable transaction and financial data, allowing businesses to gain profound insights into their customers’ behavior and preferences. Once again, statistical information from such data-driven insights is vital both for banks and their non-financial partners. For non-financial companies, such as stores, this data-driven approach is essential for refining their products and marketing strategies. They get to review the decision-making of their clients to understand what aspects of their behavior they should target. Banks and other financial organizations (for instance, in the sphere of insurance) also get massive benefits from the presented changes. These organizations can review the statistics from multitudes of websites and get much more information on user behavior in a centralized manner. This is vital because financial organizations get a chance to change their services and concentrate on some unique offerings for the average user.

Cost Savings

Many websites online don’t belong to large organizations with massive incomes. In fact, the majority of course platforms or websites for selling diverging devices are notable for being small businesses. This means building in-house financial infrastructure can be costly and time-consuming for these organizations. Even site creation is already an expensive endeavor for many of them. With embedded finance, non-financial businesses can leverage the expertise and infrastructure of financial partners. This is important for reducing development costs and accelerating time-to-market for new services. Instead of having to develop separate financial modules for their sites, many stores can now embed payment and even loan opportunities from financial partners. Since countless organizations offer easy-to-use APIs, performing a full-scale isn’t even difficult. All one has to do is add a major module and connect it to the financial accounts of the seller through comfortable user-oriented tools.

Financial Promotion and Inclusion

Many people (especially from impoverished regions) either don’t have access to financial services or deeply distrust them due to the negative experiences of relatives and friends. For instance, microfinance organizations have a negative reputation for ruining the financial status of many individuals. Embedded finance has the potential to promote financial services among underserved populations and expand access to them in certain cases. By reaching customers through familiar platforms, such as social media or ecommerce apps, financial organizations can make many services more acceptable for the average user. More importantly, these services are likely to appeal more to people who might have been excluded from traditional banking organizations. What’s the core aspect here? Embedded finance tends to include sector-specific programs. This means small businesses or low-income customers can get access to low-interest loans designed specifically for certain websites. In this way, more people would be willing to take out loans and improve their credit history. One successful loan may then lead to others, turning the clients into happy consumers of financial products.

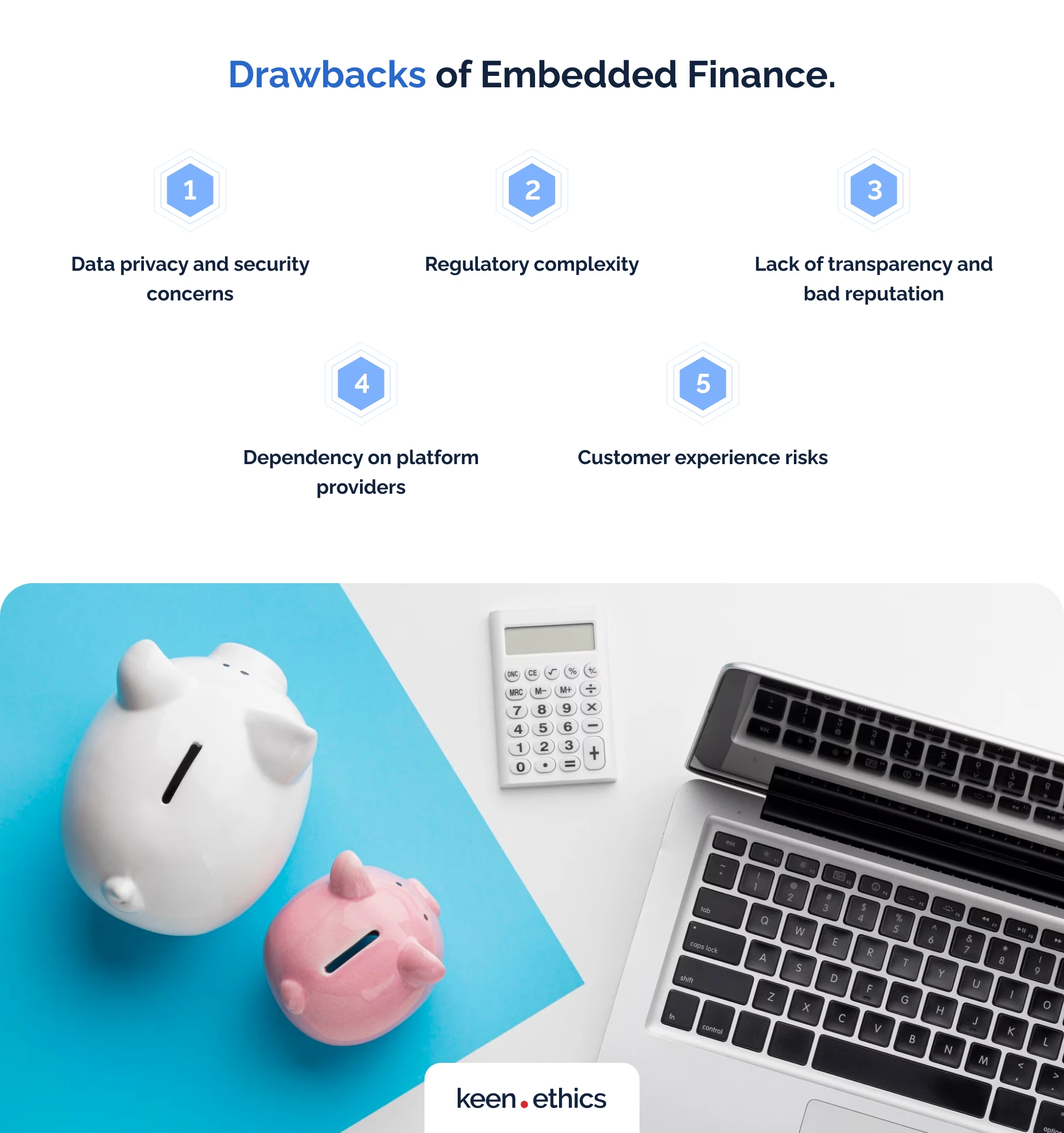

Drawbacks of Embedded Finance

While most embedded finance examples show only the positive aspects of investing in the key technology, we can also outline some negatives of the presented approach. Here are the key aspects you need to consider:

Data Privacy and Security Concerns

All embedded finance companies share their code across many websites. They take customer data from third-party providers and deliver it to them on a constant basis. Such an approach is essential if you want to offer banking services on diverging websites. After all, the clients either have to share their data or connect the banking accounts within the non-financial platforms. This issue raises concerns about data privacy and security breaches. Modern embedded finance greatly raises the risks of massive data breaches. Why is this so relevant? Embedded finance exposes financial services across multiple platforms, raising risks in two ways.

Firstly, the amount of code necessary for embedded platforms is larger than in the case of a simple website. Many errors can creep in such conditions: testing is more difficult to perform due to the volume of work. Secondly, a big problem is the interaction between non-financial platforms and embedded frameworks. Some bugs may be a result of malignant connections between non-financial site code and the embedded frameworks. Since the key interactions are impossible to test properly, there’s always a massive risk of tremendous errors stemming from the current approach to embedded finance. Isabelle Castro Margaroli, a journalist for the Fintech Nexus website, reports that security researchers have found multiple massive problems with the long-term safety of the existing embedded finance platforms. They all have easy-to-exploit vulnerabilities.

Regulatory Complexity

The aforementioned security problems inevitably lead to major attention for the embedded finance companies from the government. To protect the users from potential problems, they have to intervene and thoroughly review all the potential cases of data breaches. In this light, the number of regulations for embedded finance technologies is growing. One also has to consider the strictest versions of the traditional regulations for the banking sector. All this means the integration of financial services within non-financial platforms can end in complex regulatory challenges, as multiple industries’ regulations may overlap and require compliance, creating a legal and operational burden. The embedded finance developers are caught between the need to create products with strong regulatory oversight for finance, Internet-based technology, and, specifically, embedded finance. Likely, this sector is among the most complex when it comes to satisfying the demands of government officials.

Lack of Transparency and Bad Reputation

The key goal of any individual who creates an embedded platform is to maximize profits. Regrettably, we have many embedded finance examples that showcase the dark side of this technology. These projects aren’t cheap and target underserved populations. In this light, it makes sense to invest in the frameworks that obscure particular aspects of the relevant contracts for the users, for instance. Some companies do everything to make their services as confusing as possible for the average user to maximize profits. In cases when unfair play isn’t in action, these problems may nonetheless appear. The reason is simple: many embedded finance decisions are spontaneous, and the clients can misunderstand the essence of their loans. What does this lead to? All this leads to potential confusion, hidden fees, or inadequate consumer protection. Such a situation ends in a negative reputation for the sector, with many people considering it as a potential scam rather than a high-quality opportunity for purchasing goods and services.

Dependency on Platform Providers

Many stores also get major downsides from the integration of embedded finance. The dependence on third-party platforms is within the definition of embedded finance. What does this potentially end in? Businesses relying heavily on embedded finance may become overly dependent on platform providers, limiting their flexibility to switch partners or negotiate better terms. Many companies develop their whole software around certain payment platforms. Banks, regrettably, use this factor to worsen the situation for their users: they tend to raise fees, knowing that the clients can’t switch to some other service reliably. This dependence can lead to massive expenditures for embedded finance. Dependency manifests in the inability to add new features and push the relevant products toward the client’s needs, too. Since payment platform development fully depends on banks and other financial organizations, you can’t add the things your customers want from a relevant platform.

Customer Experience Risks

The final problem of all embedded finance is code compatibility. When creating a site, non-financial web developers have to consider one large problem: it’s possible that embedded finance features would cause unexpected bugs. Apart from the aforementioned security problems, this can also end in a low-quality user experience. The bugs may have no impact on security, but they can disrupt the interfaces. For example, the transition between a site checkout and the embedded finance service may be unaesthetic. All this affects the overall customer experience and potentially results in customer dissatisfaction. If you have a luxury service, all aspects of it should have a perfect look. Without it, the likelihood of a negative attitude toward your site will be extremely high. All this inevitably ends in larger expenditures for the relevant service. If you intend to use embedded finance, it’s essential to pay for improved integration. This factor raises the site usage costs and boosts the amount of time necessary for delivering certain features.

Embedded Finance Trends for 2023

Now that we understand the positive and negative sides of embedded finance, it’s time to review the embedded finance trends. Here are the key aspects you need to consider for success:

Increased Use of Blockchain Technology

Blockchain is one of the core financial technology trends in the modern world. The technology is notable for its high level of security and transparency. It’s not surprising that an increasing number of people are willing to use this technology en masse. As blockchain becomes more widely adopted, we may see more financial products and services leveraging this technology. This could include things like decentralized lending platforms and digital identity verification tools. Are there any examples of embedded finance based on the usage of this technology? Yes! For instance, PayPal is actively considering the adoption of blockchain technologies within its core platforms. More and more services are using the blockchain actively, according to Mercuryo, a major cryptocurrency service and analytics website.

Integration with IoT Devices

With the rise of smart homes and connected devices, there’s an opportunity for financial services to be seamlessly integrated into these ecosystems. For example, insurance companies could offer personalized coverage based on data from a user’s smart home sensors. Another interesting option is to create an automated delivery of foods based on the analysis of the refrigerator contents. The possibilities are endless with modern IoT devices. Your key goal here is to connect financial services to a maximum number of platforms. Both insurance and loan/payment processing services can benefit from such an approach.

Growth of Embedded Finance in Emerging Markets

What was the key problem for many developing countries in the preceding 20 years? It wasn’t even the lack of funds but the absence of accessible technologies. With the advance of cheap smartphones (many models cost between 70 and 120 dollars), it’s now possible to achieve widespread Internet coverage even in the poorest regions of Africa. This, in turn, creates a major revolution in the approach to embedded finance within developing regions. For instance, the IMF (International Monetary Fund) reports that Africa now needs strict cryptocurrency regulation due to the recent boom in the adoption of this technology. As more people gain access to smartphones and the Internet, there’s a growing demand for financial services in emerging markets. Embedded finance can help meet this demand by providing low-cost, accessible financial products and services. Many financial opportunities within embedded finance target newcomers. Thus, embedded finance integration is a perfect framework for attracting first-time users to the relevant markets.

Expansion of Embedded Finance beyond Traditional Industries

The most common creators of embedded finance platforms are financial organizations. These platforms typically stem from the banking or insurance companies. In the future, we may see more non-financial companies exploring the possibilities of integrating financial services into their products. This could include everything from healthcare providers offering financing for medical expenses to retailers delivering installment plans for purchases. Why is this such a common trend? The reason is simple: many non-financial organizations have reliable clients to whom they can give money, for example, without fearing non-repayment. This approach leads to better service coverage, as non-financial organizations may give loans at a lower interest, for instance. With the advance of cryptocurrencies and digital payment, the creation of such non-financial landing or payment frameworks becomes easier for all involved parties.

The Prospective Outlook for Embedded Finance

The long-term prospects of investments in embedded finance are extremely positive for all involved parties. In this regard, the growth of the sector is, more or less, inevitable. As Statista, one of the largest statistics websites, reports, embedded finance saw a three-fold increase in venture capital investments in 2021. This sector is now attracting an increasing number of users and, of course, business partners. Indeed, COVID-19 led a significant part of the aforementioned growth. Nonetheless, the benefits of embedded finance are too large to ignore. This means that venture capital investments will see steady growth in the upcoming years. In these conditions, the number of embedded finance users will grow. As a result, the investments within this sector make sense. It’ll offer massive long-term benefits to all the key investors in the upcoming years.

Optimal Embedded Finance Options for Your Company

Do you want to create a high-quality embedded finance product for your firm? In this regard, our company is among the best development firms. We’ve developed multiple fintech projects, which include many aspects of embedded finance. Among the examples of embedded finance is the BankerAdvisor site, which collects a lot of vital data about existing bank fees. We also have other projects that embed financial information. You can contact us to deliver a free estimate of your project and offer a full analysis of your embedded finance idea. Key reports indicate an almost five-times growth for the embedded finance sector: it’ll grow from 54 billion U.S. dollars in 2022 to 248 billion in 2032.

Conclusion

So, why is embedded finance important? In our opinion, the key reasons to promote it include user comfort and increased coverage. These services make the user experience better and, more importantly, boost the number of people willing to try out some financial services. We believe embedded finance is the future of the banking and insurance sectors. Companies in this sector work with many non-financial services, and their integration into them can be beneficial.

Common Questions About Embedded Finance

What is open banking?

Open banking is a financial model allowing third-party access to bank data and services. This approach fosters innovation and enables customer empowerment through advanced customization.

What is embedded finance?

Embedded finance integrates financial services seamlessly into non-financial platforms to enhance convenience and accessibility for users and businesses.

How do banking as a service and embedded finance differ?

Banking as a service enables third parties to offer banking services. In turn, embedded finance integrates financial services into non-financial platforms directly.

Why will embedded finance be big in the next five years?

Embedded finance will grow due to increased digitalization, customer demand for seamless experiences, and partnerships between fintech and non-financial industries.

Is there a specific use case for embedded finance?

Yes, a specific use case for embedded finance is offering instant point-of-sale financing options within ecommerce platforms or stores.

What opportunities are there in embedded finance?

Opportunities in embedded finance include enhanced user experiences, new revenue streams for businesses, and expanded financial inclusion possibilities.

If you want to capitalize on this trend, don’t hesitate to contact us: we know how to implement this technology.